Your ISA has changed

When you turn 18, the Junior ISA (JISA) invested for you becomes an adult Individual Savings Account (ISA), known as your CT ISA and you have responsibility for the account.

This will happen automatically so don’t worry – we will take care of it.

What is an ISA?

An ISA is an account that acts as a wrapper to hold savings or investments reducing the tax you might need to pay now, or in the future.

If you live in the UK, each tax year (6 April to 5 April the following year), the Government gives you an annual allowance which is how much can be contributed into ISA(s) in your name.

When you held a Junior ISA, this allowance was £9,000, and the good news is with an adult ISA, this more than doubles to £20,000 per year. You can see other key differences between an ISA and Junior ISA below.

CT Junior ISA | CT ISA | |

|---|---|---|

Minimum Opening Investment Amount | £1,000 | £2,000 |

Annual Account Charge | £25 + VAT | £60 + VAT |

Dealing Charge | Postal transactions – £12 dealing charge Free if done online | Postal transactions – £12 dealing charge Free if done online |

Investment Allowance | £9,000 per tax year | £20,000 per tax year |

Friends and family can invest | ||

Investment Options | 9 Investment Trusts | 9 Investment Trusts |

What we need from you?

We’re required to hold the National Insurance Number for ISA investors. To provide us with this, register for our online Investor Portal at ctinvest.co.uk/login. You’ll be asked to provide your National Insurance Number when you log in or you can send us a secure message. This is also where you can manage your investment.

Providing proof of your identity

We need you to send us documents to prove your identity and where you live. This is an important step as it ensures we know who you are, and that only you have access to your funds. Until this step is complete, you cannot take money out or add any new investments.

You may also want to send us proof of your bank details. This allows us to make future withdrawals directly into your bank account and/or set up future regular investments from that account.

A list of what documents we can accept can be found in the FAQs below

Starting a Direct Debit

If anyone had an active Direct Debit arrangement for regular contributions or to pay account fees on your Junior ISA, this will have stopped.

If you now want to set up your own Direct Debit to invest monthly or pay fees, you can do this on our investor portal.

If anyone else wants to make contributions, it’s not possible to do this online, but you can do this using an ISA top-up and Third party donor form. Simply complete these and send them to us together by post.

Let's talk about risk

All of our savings plans involve a level of risk and the value of your investments can go down as well as up. The level of risk will depend upon the underlying investments that you choose to hold in the plans. You need to be comfortable that you may not get back the original amount invested. Tax allowances and the benefits of tax-efficient accounts are subject to change and tax treatment depends upon your individual circumstances.

Frequently asked questions

You can have more than one ISA account allowing you flexibility. For example, you could invest your full £20,000 allowance in a Stocks and Shares ISA or you could split the allowance between a Stocks and Shares ISA and a Cash ISA. Please note even if you have more than one account your allowance is still £20,000 per tax-year (allowance correct for 2025/26 tax-year).

Payments are normally made from the ISA account holder. We can accept payments from third parties however we will require a letter, signed by them and sent along with the payment, that confirms that the money is being irrevocably gifted to the ISA account holder. We may also be required to verify the identity of the payer (for example, a certified copy of their current passport or driving license for identity and a copy of a bank statement or utility bill as proof of address). If someone else is planning to make a payment into your ISA you may want to contact our Investor Services team (0345 600 3030 or +44 1268 447 407 if you’re overseas, lines are open weekdays 9am-5pm) in advance of the payment being sent to check if anything further will be required.

As the account holder (you can only have one account holder for an ISA) you can top up through the online Investor Portal using a debit card. Alternatively, you can send us a cheque in the post along with the relevant Top-Up Form.

Your money is invested on the next available dealing day after receipt of your payment (subject to online dealing cut-off times, up to 11:59pm).

The proof needs to be pre-printed by your bank and show:

- Your sort code

- Your account number

- The name of the account holder(s)

This is normally a pre-printed pay-in slip (which is usually found in the back of your cheque book but may be provided by your bank/building society separately) or cancelled cheques (i.e. a blank cheque that you have scored through so that it cannot be used). A cancelled cheque is sometimes referred to as a spoilt cheque or a voided cheque.

There is no tax to pay on any return on your investment, including dividends or interest received. You’ll also pay no capital gains tax (CGT), which may be relevant if you have used up all your annual CGT allowance.

To verify your identity, we can accept

- Valid passport

- Valid photocard driving licence (full or provisional)

- Recent evidence of entitlement to a state or local authority-funded educational or other grant

- Most recent HM Revenue and Customs Tax Coding Notification, Assessment or Statement (dated within the last year). If you are working and paying tax, the HMRC will send you a copy of your tax coding notification on request.

- A government-issued document that incorporates your full name and photograph and either your residential address or your date of birth.

We then need something that has been sent in the post to your residential address.

- A bank or debit card statement which has been issued within the last three months (but not ones printed off the internet). If you don’t normally get these sent in the post, if you contact your bank, they can usually send you a one-off statement.

- Utility bill issued within the past three months (but not ones printed off the internet)

- Valid photocard driving licence (full or provisional)*

- Recent evidence of entitlement to a state or local authority-funded educational or other grant*

- Most recent HM Revenue and Customs Tax Coding Notification, Assessment or Statement (dated within the last year)*

- A government-issued document that incorporates your full name and photograph and either your residential address or your date of birth*

* We need two documents so you can’t use the same document to confirm both your identity and your address. To verify your bank details, we need something from your bank which has your sort code, account number and account name printed on it e.g.

- A bank statement which has been issued within the last three months (but not ones printed off the internet). If you don’t normally get these sent in the post, if you contact your bank, they can usually send you a one-off statement. We can accept the same statement as both proof of your bank details and proof of your address.

- A voided cheque (in other words, one that you have scored through and written VOID across it so that nobody could use it)

- A pre-printed pay-in slip

We don’t recommend that you send us originals of personal documents in the post. However, you can send us certified copies instead.

Pre title lorem ipsum

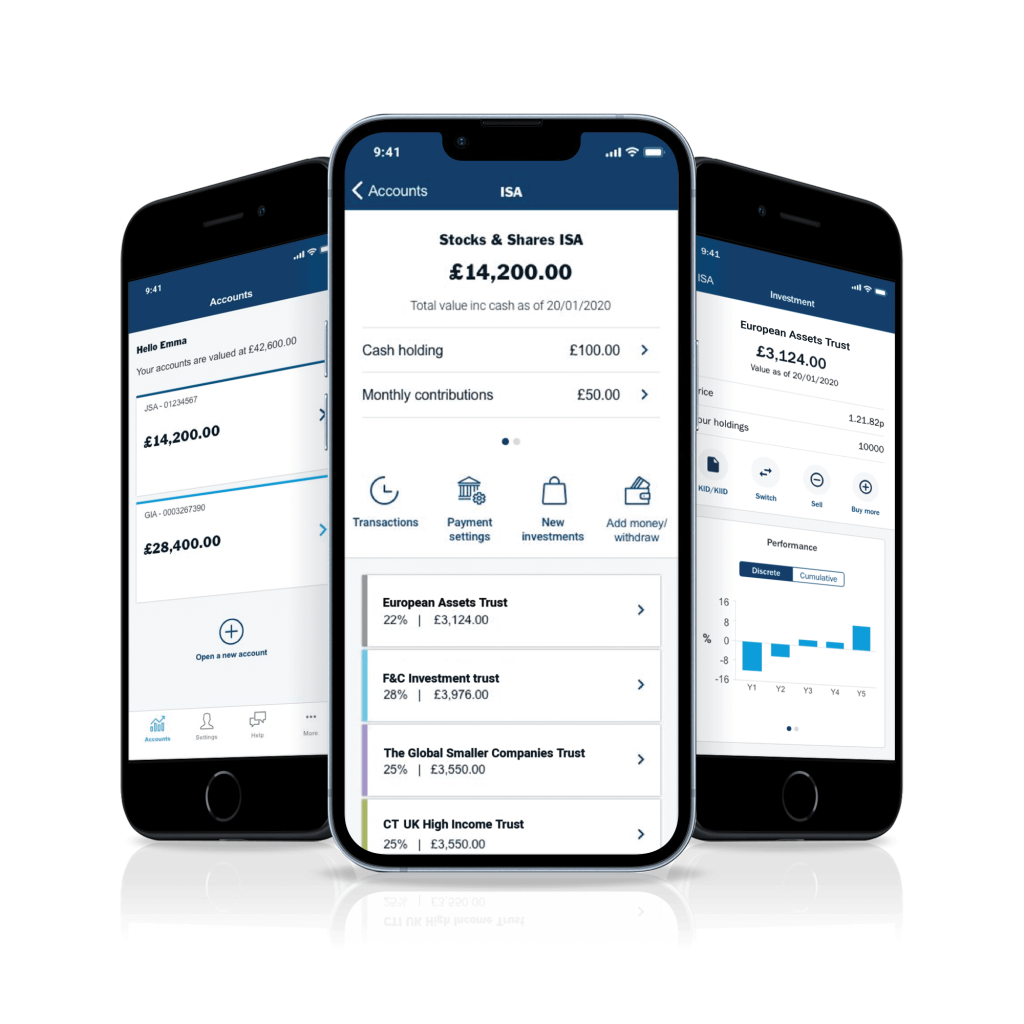

Manage your investments on

the go

Manage your investments on the go

With our App you can:

– Make changes to your investment choices

– Add cash to invest later, or withdraw cash

– Make lump sum investments

Search 'CT UK' to download the app